I’ve spent enough time watching robots freeze because their cloud latency spiked to see that “democratization” is often just marketing speak for “we need more GPUs.” The real story here isn’t the money; it’s the industrial consolidation of compute, capital, and distribution into a single, unassailable moat.

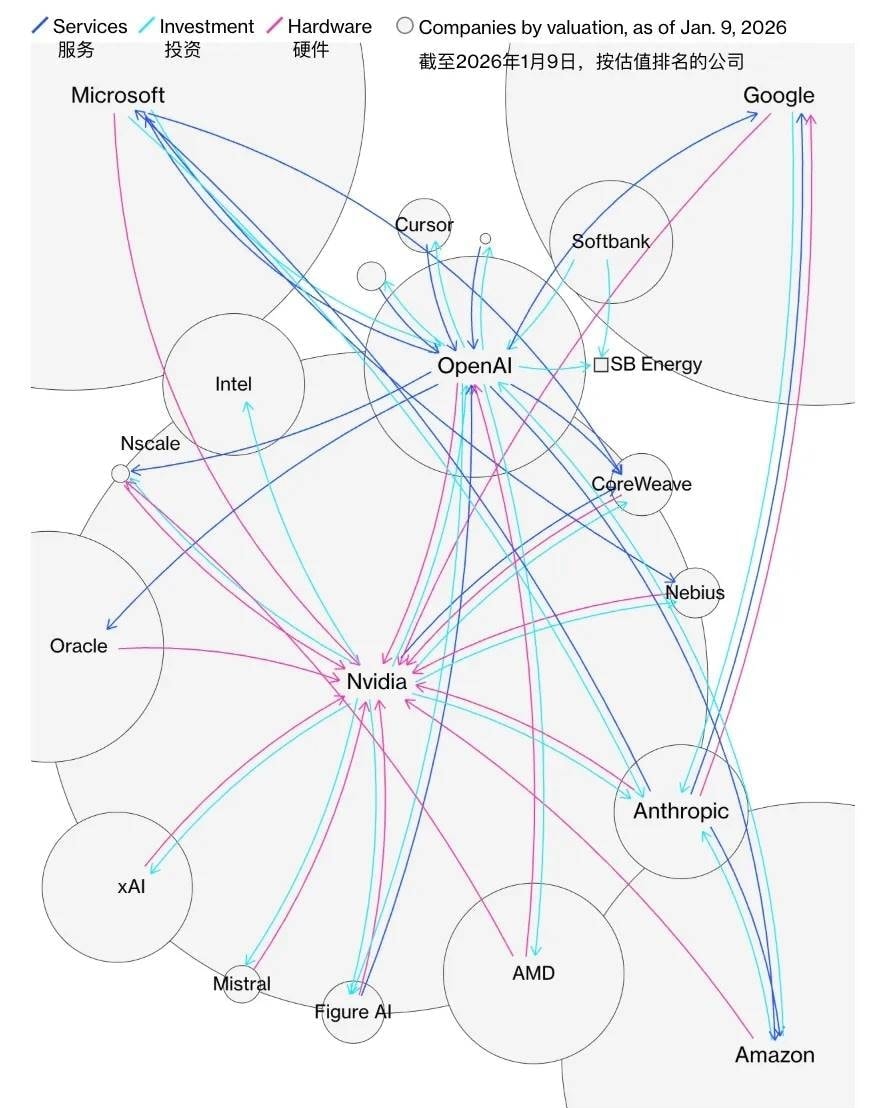

On February 27, OpenAI announced it had raised $110 billion in new funding. The round includes $30 billion from SoftBank, $30 billion from Nvidia, and $50 billion from Amazon, valuing the company at $730 billion pre-money.

This marks the largest single financing deal to date in the AI sector.

I’ve seen demo videos that look flawless until the Wi-Fi drops; this scale of capital doesn’t fix physics.

Officially, the funds will be used to expand artificial intelligence infrastructure construction, aiming to accelerate the democratization of AI.

Sam Altman outlined the specific areas of cooperation with the three partners on X:

- Nvidia: Responsible for providing underlying computing power, offering continuous and scalable training and inference capabilities centered around GPUs and next-generation accelerators;

- Amazon: Providing cloud infrastructure and global deployment capabilities to support OpenAI’s model delivery and commercialization across multiple regions and industry scenarios;

- SoftBank: Taking on a capital and ecosystem role, driving OpenAI’s expansion into broader industrial systems through long-term financial support and the integration of industry resources.

Additionally, as an existing shareholder, Microsoft did not miss out.

The two parties released a joint statement confirming that their previous cooperative relationship remains unaffected. Microsoft Azure continues to be the exclusive cloud service provider for OpenAI’s API, and Microsoft retains exclusive licensing and access rights to the intellectual property of OpenAI’s models and products.

I think when three giants lock arms, the unit economics for anyone else become impossible to justify.

At this moment, three of the most critical AI resource lines—upstream computing power, cloud infrastructure, and long-term capital—have been tied together in a single move.

The Capital Stack: Amazon, Nvidia, and SoftBank

I read the filing on this round, and what stood out to me was not just the headline number, but the specific strings attached to the cash. Amazon led with $50 billion, but that money is conditional. They are putting in an initial $15 billion, with another $35 billion pending “specific conditions.” Insiders say those conditions likely involve OpenAI “achieving AGI” or a successful IPO.

There is also a peculiar clause regarding Microsoft: once AGI is achieved, Microsoft loses access to the technology. Meanwhile, OpenAI is committing to a new “stateful runtime environment” on Amazon’s Bedrock platform. They’ve promised to consume roughly 2 gigawatts of Trainium chip compute power for Frontier and stateful workloads. This expands their previous $38 billion deal; over eight years, OpenAI plans to spend about $100 billion in cloud resources on AWS.

Amazon CEO Andy Jassy noted that the world’s two largest AI labs are heavily utilizing Trainium: besides OpenAI, that other lab is Anthropic. Amazon has already invested billions in Anthropic and built an $11 billion data center campus in Indiana (“Project Rainier”) for them. Yet, they insist this new deal won’t alter their relationship with Anthropic.

In the field, conditional capital tied to AGI milestones feels like a bet on physics, not engineering. What I watch for is aWS lock-in at 2 gigawatts of Trainium limits our ability to switch infra if costs spike.

Nvidia came in second with $30 billion. Rumors of a $100 billion investment were scaled back, but Jensen Huang previously debunked claims that Nvidia was abandoning OpenAI:

We are putting significant capital behind them; I believe in OpenAI. The work they are doing is incredible.

Now, the $30 billion is here. Under this agreement, OpenAI commits to using 2 gigawatts of training capacity on Nvidia’s Vera Rubin system, plus an additional 3 gigawatts for inference tasks (likely GPUs). Nvidia is effectively funding OpenAI to buy its own chips—a classic “circular investment” logic that keeps the hardware vendor in the driver’s seat.

I think circular investments keep chip margins high while pushing deployment risk onto the model builders. In the field, vera Rubin capacity reservations are good for Nvidia’s backlog, not necessarily for our unit economics.

The third investor is SoftBank, which also contributed $30 billion. Official announcements state this will be disbursed in three installments: April, July, and October 2026. SoftBank Chairman Masayoshi Son expressed confidence in the growth trajectory:

Through this additional investment, we will accelerate OpenAI’s research and ecosystem expansion while advancing our own AI strategy.

Media reports suggest SoftBank is also acting as a “matchmaker.” Insiders indicate OpenAI expects to secure approximately $10 billion in Series I equity financing, with commitments finalized next month. These investors—likely sovereign wealth funds and investment firms—are speculated to come through SoftBank’s bridge.

The Azure Tie Holds, But the Basket Diversifies

I read the statement carefully: Microsoft keeps its “core status” and exclusive cloud rights for the stateless API. They still get a cut even if we run workloads elsewhere. This isn’t just partnership; it’s a financial stranglehold disguised as support.

What I watch for is exclusive contracts lock in costs regardless of market competition. I think revenue sharing on third-party clouds is a tax on flexibility.

Yet, the math tells a different story about dependency. OpenAI is committing $100 billion to AWS over eight years and adopting Amazon’s Trainium 3/4 chips. This isn’t just diversification; it’s an admission that Azure alone cannot feed the beast. They are actively breaking the monopoly, even if Microsoft retains the IP rights.

The Circular Economy of Compute

This financing structure is textbook circular logic. Nvidia sells the chips and buys the equity. Amazon sells the cloud and buys the equity. OpenAI takes the cash to buy more chips and clouds from those same investors. It moves money from “investment expenditure” on one balance sheet to “operating revenue” on another, inflating stock prices while locking in future market share for the suppliers.

Altman dismisses the criticism, saying it only makes sense if new revenue flows into the ecosystem. But I see a balance sheet trick that boosts valuations without solving unit economics.

In the field, circular financing inflates stock prices but hides real operational risk. What I watch for is suppliers betting on their own customers is a conflict of interest.

The cash pile is now roughly $150 billion, combining this round with existing reserves. Yet, positive free cash flow isn’t expected until 2030. That’s nearly five years of burning capital to chase scale. The user numbers are impressive—900 million weekly active users and 57.2 billion monthly visits—but the cost to serve them remains opaque.

Anthropic just secured $30 billion, pushing its valuation toward $380 billion. The arms race is accelerating, not cooling down. OpenAI has loaded the ammunition, but whether this capital translates into deployed utility or just more expensive demos remains to be seen.

Comments

Sign in to join the discussion and leave a comment.

Sign in with Google