The automotive sector is a critical frontier for AI infrastructure, yet it presents a unique paradox: massive revenue potential colliding with intense margin pressure. As I followed Nvidia’s latest earnings report, one detail stood out immediately—the company’s guidance for automotive vertical revenue hitting $5 billion this year (approximately 36 billion yuan). This figure underscores the scale of the opportunity, especially following the launch of its next-generation autonomous driving chip, Thor.

However, the market’s reaction tells a different story. Despite reporting record-breaking financial results that exceeded expectations, Nvidia’s stock plummeted 8.48%, wiping out $271.6 billion (approximately 1.9 trillion yuan) in market capitalization overnight. This sharp decline suggests investors are questioning whether the current era of outsized profitability is sustainable as competition intensifies and hardware cycles evolve.

I think high market cap drops signal investor anxiety about future margins. As a builder, automotive revenue guidance shows strong demand for autonomous tech. Personally, stock volatility reflects uncertainty around Nvidia’s long-term dominance.

Has the end come for Nvidia’s monopoly on profits?

The Margin Squeeze Behind the Record Revenue

I’ve been tracking Nvidia’s fiscal 2025 fourth-quarter earnings, and while the headline numbers are staggering, the underlying story is about a company hitting its first real speed bumps. Consistent with most quarters over the past three years, Nvidia’s report surpassed Wall Street expectations, but the details reveal a shifting landscape for developers and investors alike.

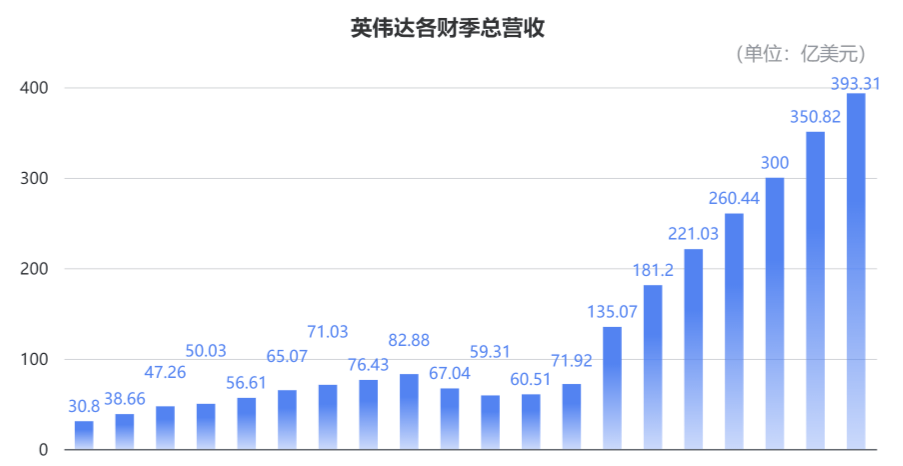

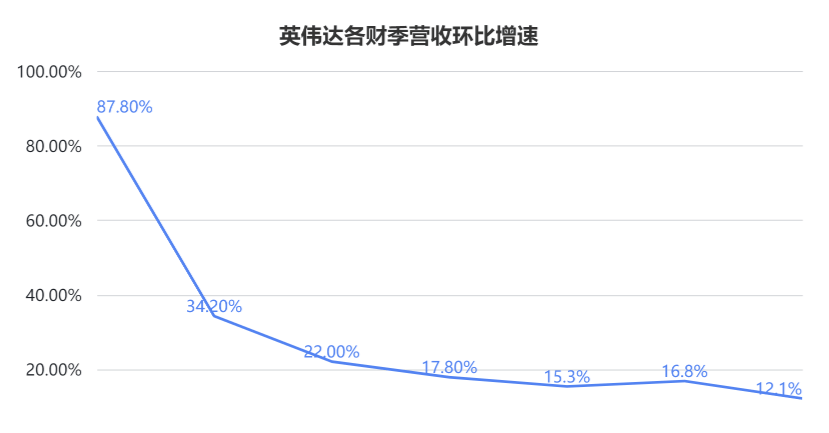

Operating revenue for the quarter hit $39.3 billion (approximately 285.3 billion yuan), marking a 78% year-over-year increase and a 12% quarterly jump—a new historical record.

However, this beat against the analyst consensus estimate of $38.1 billion (approximately 276.7 billion yuan) came with a caveat: the quarter-over-quarter growth rate slowed further, aligning with predictions. This deceleration is one reason for Nvidia’s recent stock price volatility.

For the full fiscal year 2025, total operating revenue amounted to $130.5 billion (approximately 947.5 billion yuan), representing a massive 114% year-over-year growth.

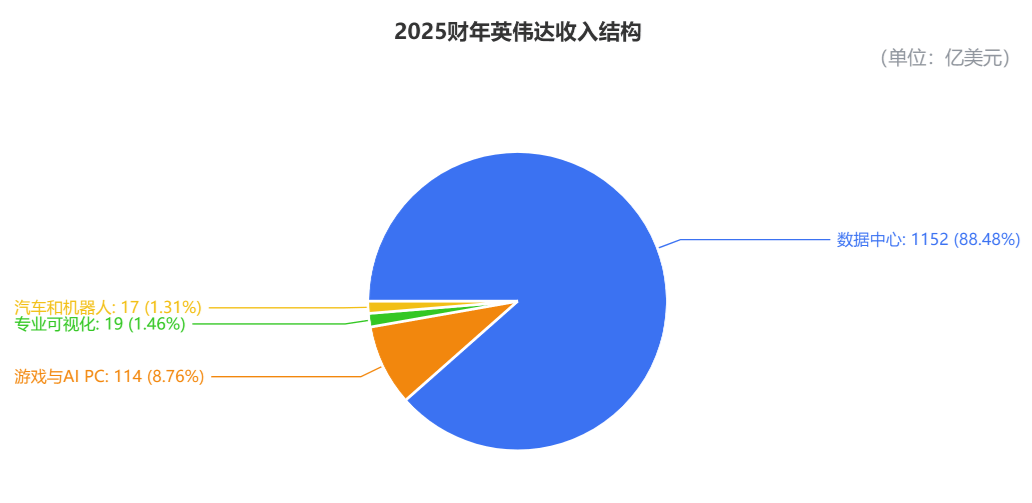

Breaking down the revenue by business type reveals where the money is actually coming from:

Data Center remains the undisputed king, generating $115.2 billion (approximately 836.4 billion yuan) annually, up 93% year-over-year. This accounts for 88% of total revenue, an increase of 10 percentage points compared to the previous year.

The Automotive and Robotics segment generated $1.7 billion (approximately 12.4 billion yuan). While this is only 1.31% of total income—the smallest share among the four categories—it experienced the fastest growth, surging by 103% year-over-year. Nvidia attributed this primarily to the continued expansion of autonomous vehicles.

Full-year revenue from Gaming and Professional Visualization was $11.4 billion and $1.9 billion (with another segment at $1.7 billion), respectively, showing modest year-over-year growth rates of 9% and 10%.

Nvidia also confirmed that the Blackwell architecture has entered mass production. In this first delivery quarter, sales revenue reached $11 billion (approximately 79.9 billion yuan), making it the fastest-growing product in Nvidia’s history.

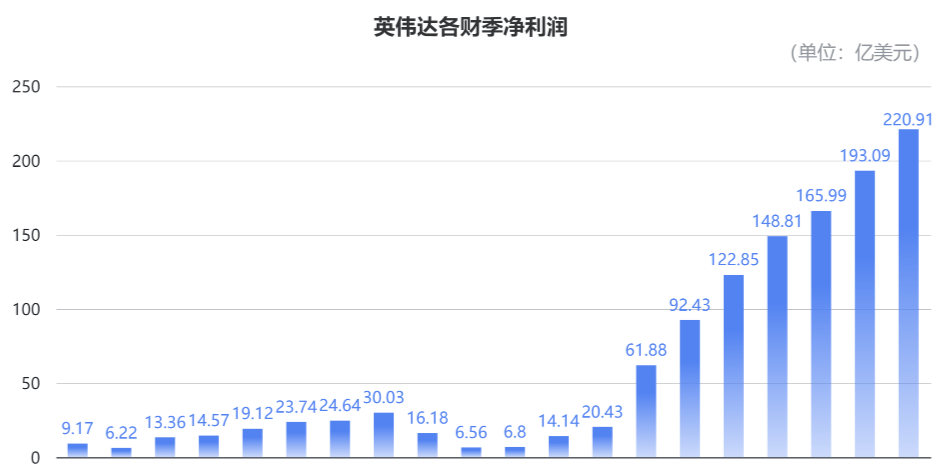

In terms of profitability, net income for the fourth quarter was $22.09 billion (approximately 160.4 billion yuan), up 80% year-over-year and 14% quarter-over-quarter. Full-year net income reached $72.88 billion (approximately 529.1 billion yuan), a 145% increase year-over-year.

The gross margin for the fourth quarter was 73%, slightly below the expected 73.5%. This represents a year-over-year decline of 3 percentage points and a quarter-over-quarter drop of 1.6 percentage points; however, the full-year gross margin stood at 75%, up 2.3 percentage points year-over-year.

Against the backdrop of overall financial metrics rising and exceeding analyst expectations, the decline in fourth-quarter gross margin stood out prominently.

Nvidia explained that this was due to newer data center products being more complex and expensive. Previously, delays in deploying data centers by major tech companies—caused by overheating issues with Blackwell chips—and increased production costs led Nvidia to offer some concessions.

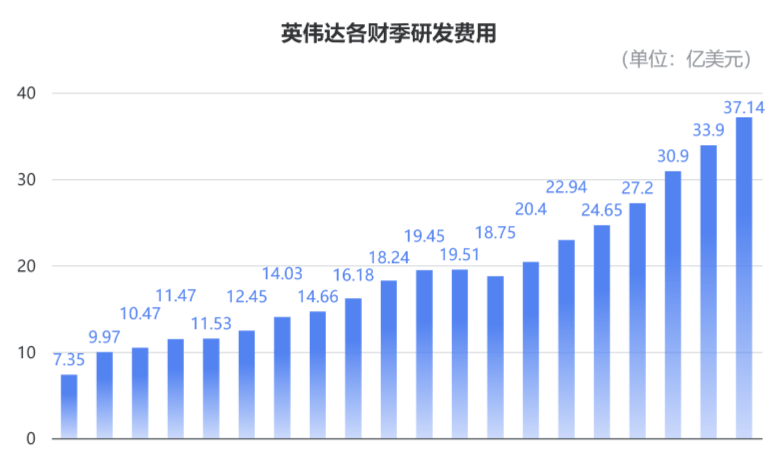

Furthermore, due to bottlenecks in product progress, Nvidia’s enthusiasm for R&D investment reached unprecedented levels. R&D expenses for the fourth quarter totaled $3.714 billion (approximately 27 billion yuan), a year-over-year increase of 50.7% and a quarter-over-quarter rise of 9.6%.

Full-year R&D expenses for fiscal 2025 reached $12.914 billion (approximately 93.8 billion yuan), up 48.9% year-over-year.

I think blackwell’s rapid sales prove demand is still insatiable. As a builder, margin compression suggests hardware complexity is outpacing pricing power. Personally, r&D spending spikes indicate the next generation of chips will be even more expensive to build.

Overall

Two Generations of Auto Chips Generate $36 Billion, but Nvidia’s Profitable Era Is Ending

As a developer watching the infrastructure shift underpin autonomous systems, I see Nvidia betting heavily on the next wave of in-vehicle compute. While their recent performance has been stellar, the company is signaling that its golden era of explosive growth may be winding down. The narrative is shifting from pure AI dominance to sustaining momentum in automotive and robotics verticals.

This remains a positive year-end performance that exceeded expectations.

Nvidia has already provided guidance for the first quarter of fiscal 2026:

Amidst unprecedented enthusiasm for intelligent driving and continuously rising demand for in-vehicle computing power, Nvidia maintains an optimistic outlook on the autonomous driving market and its position within the industry:

- Revenue for Q1 fiscal 2026 is expected to be $43 billion (approximately 312.2 billion yuan), with a variance of ±2%;

- Automotive vertical revenue for full-year fiscal 2026 is projected to grow to $5 billion (approximately 36.2 billion yuan).

This is nearly three times last year’s automotive-related revenue, and this figure includes robotics contributions as well.

I think the $43B Q1 guidance suggests demand hasn’t cooled yet. As a builder, doubling down on auto chips is a high-stakes pivot. Personally, robotics inclusion in auto revenue blurs the lines for developers.

However, does reality truly support Nvidia’s ambitions?

What Are Nvidia’s Key Moves This Year?

Nvidia’s confidence hinges on its newly launched autonomous driving chips. I’ve been tracking how these hardware shifts impact the developer ecosystem, and the fragmentation here is notable.

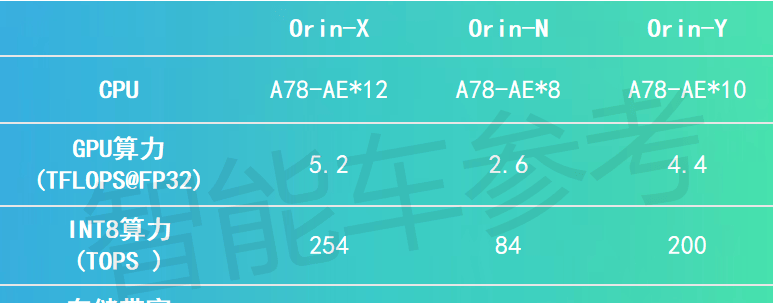

Two models from the Orin series are available: Orin-N and Orin-Y.

The Orin-N targets the low-price market, competing with chips such as Qualcomm’s SA8650 and Infineon’s TDA4VH. However, with a computing power of 84 TOPS, its position seems somewhat awkward compared to the newly released Orin-Y.

Orin-Y focuses on cost-effectiveness, offering 200 TOPS of computing power—slightly lower than the Orin-X’s 254 TOPS. By streamlining certain specifications, costs have been significantly reduced, making it a viable alternative to the Orin-X and appearing more competitive relative to the Orin-N.

I think fragmented SKUs like Orin-N and Y complicate our tooling support. As a builder, developers need clear migration paths from older Orin generations.

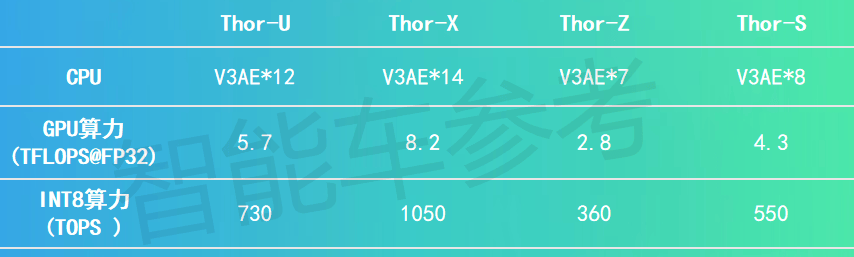

Additionally, there is Thor, the next-generation chip that has been long-awaited.

According to Jensen Huang, Thor’s processing capability is 20 times that of its predecessor, Orin.

This generation of chips is based on the latest Blackwell architecture, integrating multiple dedicated computing cores and utilizing TSMC’s 4-nanometer process along with CoWoS-R packaging technology.

Thor can simultaneously process data from various sensors, including cameras, radars, and LiDARs, enabling multi-modal perception and decision-making.

In 2025, Nvidia will primarily promote two Thor variants: Thor-U and Thor-X, with single-chip computing powers of 730 TOPS and 1050 TOPS, respectively. Thor-Z and Thor-S are expected to be released next year.

Personally, high TOPS numbers don’t matter if the SDK isn’t ready. I think we need stable APIs before chasing raw compute benchmarks.

Thor’s design was finalized around late 2021, and it debuted in September of the following year. However, mass production dates were repeatedly pushed back—from mid-2024 to January of this year—when Jensen Huang finally announced full-scale production at CES.

These repeated delays have directly impacted automakers’ vehicle development schedules, forcing some to alter their plans.

For example, the Xpeng P7+ was originally planned to use Thor chips. Due to Thor’s repeated postponements, it ultimately opted for the previous-generation Orin.

Such occurrences have raised market concerns regarding chip availability, and Nvidia faces the risk of losing core customers.

As the Autonomous Driving “Pie” Grows, Is Nvidia’s Share Shrinking?

China is currently one of the world’s largest automotive markets and undoubtedly one of the countries with the greatest technical potential and growth scale in the autonomous driving industry.

A significant portion of the dividends Nvidia has reaped from the automotive market comes from Chinese automakers.

When Nvidia’s Orin autonomous driving chip first entered China, domestic intelligent driving technology was developing rapidly, and vehicle intelligence had become a new battleground for competition among automakers. There was an urgent need for high-performance chips to meet computing demands.

Coincidentally, the arrival of Orin chips aligned with market needs, becoming one of the top choices for automakers looking to enhance their intelligent driving capabilities. At that time, most advanced solutions utilized dual Orin-X configurations.

However, at the current juncture, the situation is entirely different.

Admittedly, the continued growth of the automotive market, particularly the popularization of intelligent driving in China, will bring considerable opportunities to Nvidia.

The pie has grown larger, but there are more people eating from it; even those who helped bake the pie now want a slice.

Nvidia’s share is being carved up by other chip manufacturers and automakers.

Let’s look at competitors in the same track. Compared to the past, their strength is no longer comparable.

Overseas players include Qualcomm, Mobileye, and Texas Instruments.

Take the strongest competitor, Qualcomm, for instance. Its automotive business growth has been very robust, with the Snapdragon Ride Flex being positioned as a direct rival to the Orin-X.

In October last year, Ride released its “Ultimate” version, which can integrate both cockpit and intelligent driving functions on a single platform.

This version supports over 40 sensors, including multiple exterior cameras with 16-megapixel resolution and 360-degree panoramic infrared cameras for passengers.

It is adaptable to luxury vehicles, flagship mid-to-high-end models, and mass-market cars alike, having already secured public partnerships with Mercedes-Benz and Li Auto.

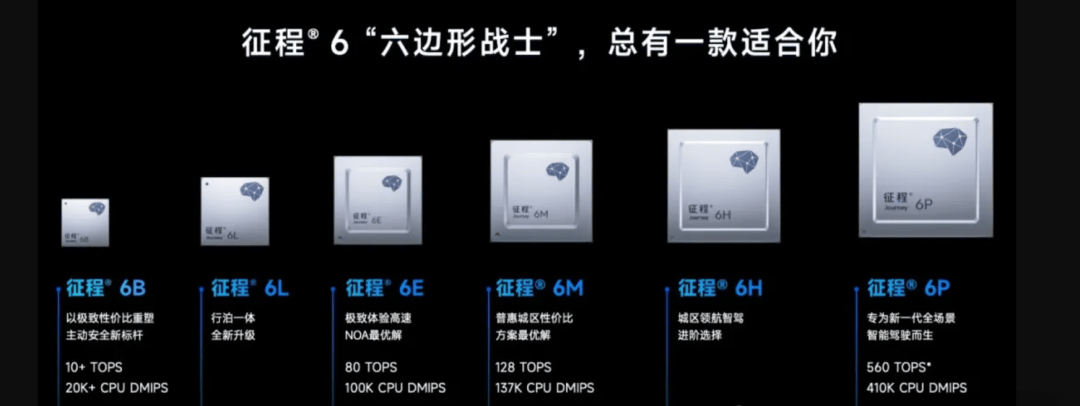

Domestically, chip manufacturers such as Horizon Robotics and Black Sesame Technologies are also gradually expanding their market share.

Taking Horizon’s Journey 6 series chips as an example, the flagship product, Journey 6P, adopts a quad-core BPU architecture and integrates 18 Cortex-A78AE processors.

A single chip can support full-stack computing tasks including perception, planning and decision-making, and control, with computing power reaching 560 TOPS—more than double that of the Orin-X.

Currently, over 7 million Journey 6 series chips have been mass-produced, with partnerships exceeding 20 automakers and brands, securing design wins for more than 100 mid-to-high-end intelligent driving models.

Beyond chip manufacturers, automakers are beginning to shift toward in-house chip development, including Xpeng and NIO, which were among the first to mass-produce vehicles using Nvidia chips.

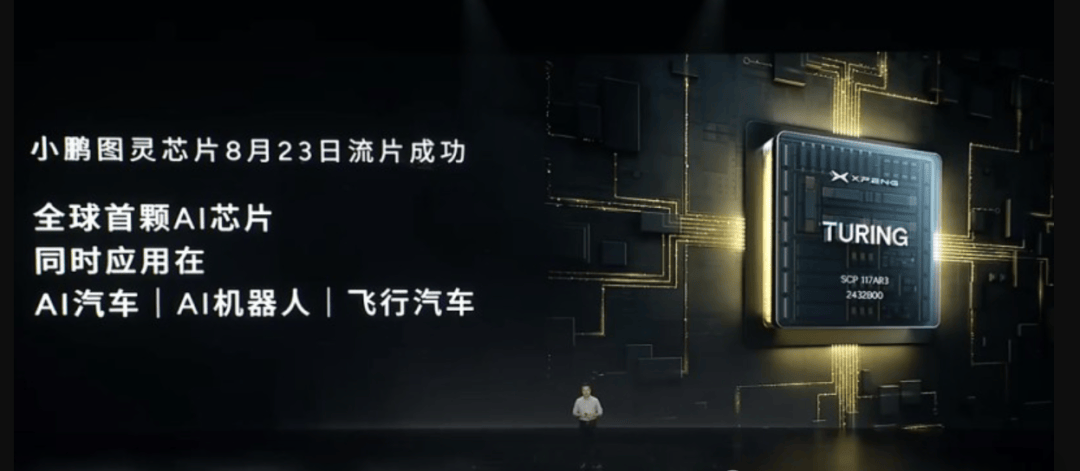

In August last year, Xpeng’s self-developed chip successfully completed tape-out (successful trial production), announcing this progress at a press conference and naming it the “Turing Chip.”

Reports indicate that this chip is customized for AI large models and can be applied to various AI hardware such as AI cars and flying cars, with computing power approximately three times that of its peers.

The “Turing” chip is expected to debut in vehicles in May this year, when Xpeng will launch a new model equipped with it.

Subsequent Xpeng models may no longer use Nvidia’s Thor chips.

According to 36Kr, NIO has also not placed orders for Thor.

Its self-developed chip, “S

As a builder, vertical integration threatens the general-purpose accelerator model we rely on today. Personally, competitors offering higher TOPS per dollar force us to re-evaluate our hardware stack choices. I think automakers building custom silicon reduces the addressable market for standard dev kits.

The End of an Era for Nvidia’s Auto Chips

NIO’s partnership with Nvidia may well conclude with the Orin chip, marking a pivot point in automotive silicon strategy. The NX9031, officially completed tape-out in July last year, stands as the world’s first automotive-grade intelligent driving chip manufactured using a 5-nanometer process. This milestone highlights the rapid evolution of hardware capabilities, yet it also signals a potential ceiling for Nvidia’s dominance in this specific segment with NIO.

Despite this shift, Thor retains a formidable market presence. It continues to power vehicles from major players including Tesla, BYD, Li Auto, Mercedes-Benz, and Toyota. However, the landscape is fracturing. According to 36Kr Auto, Li Auto is actively advancing its own chip development under the project codename “Schumacher.” This internal push aims to reduce reliance on Nvidia’s Thor, illustrating a broader industry trend where former partners are becoming competitors.

As a builder, in-house silicon offers long-term control but demands significant engineering overhead. Personally, relying on a single vendor for critical autonomous driving hardware is a strategic risk. I think the race to 5nm automotive chips raises the bar for all legacy players.

The market Thor now faces is vastly different from that of the “Orin era.” As automakers seek vertical integration, Nvidia’s profitable era in auto chips appears to be winding down.

Comments

Sign in to join the discussion and leave a comment.

Sign in with Google