The core technical claim is that OpenAI incurred an $11.5 billion net loss in the third quarter of 2025, derived by reverse-engineering Microsoft’s financial disclosures using the equity method of accounting. This figure would be falsified if Microsoft’s reported impairment or equity-based losses from its OpenAI investment were significantly lower than the $3.1 billion disclosed, or if the ownership stake used in the calculation deviates materially from the 27% cited in recent restructuring documents.

Sharp-eyed netizens discovered that OpenAI actually lost $11.5 billion last quarter!

The key point here is that this isn’t hearsay from some media outlet; it was revealed directly by OpenAI’s largest backer—Microsoft itself.

I followed the release of Microsoft’s Q3 2025 earnings report, and what stood out to me was how the accounting mechanics expose the true scale of OpenAI’s burn rate. The narrative that this is merely a “little brother” annoying his boss misses the structural reality: under the equity method, Microsoft must recognize its share of OpenAI’s operational losses directly in its own income statement.

Let’s take a look at what exactly happened.

Microsoft Takes a $3.1 Billion Hit Due to “Little Brother’s” Losses

Microsoft has undoubtedly reaped massive profits in this AI wave.

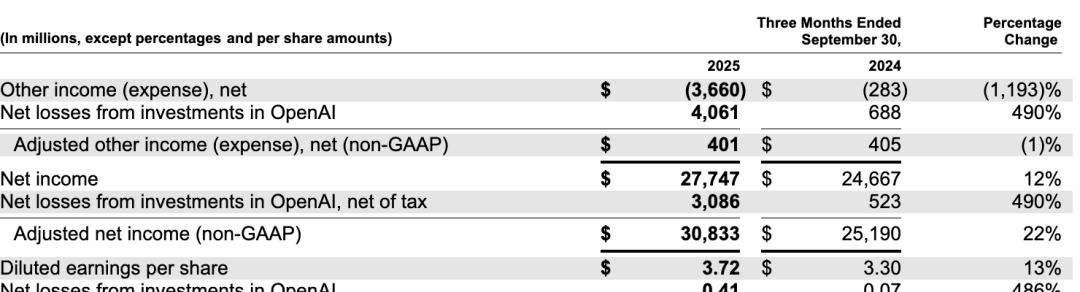

In the third quarter of 2025, Microsoft’s net profit reached $27.7 billion, up 12 percentage points year-over-year.

However, despite earning so much, Microsoft seems a bit “unhappy.”

The gist is: if it weren’t for this “little brother” dragging down performance, profits could have easily broken the $30 billion barrier this quarter!

Net income and EPS for the year were negatively impacted by losses from the investment in OpenAI, reducing them by $3.1 billion and $0.41 per share, respectively.

Wait a minute—didn’t OpenAI recently claim its IPO valuation could reach one trillion dollars?

Logically, Microsoft’s stake should be worth a fortune. So why the loss?

Actually, this isn’t how the accounting works.

On page 9 of the earnings report, Microsoft provided an official explanation:

The investment is accounted for using the equity method. Our share of OpenAI’s income or losses will be reflected in the “Other Income (Expense), Net” line item in our financial statements.

This sentence is crucial, especially the term “equity method,” which conveys significant information.

It means Microsoft cannot simply adjust its book value based on market valuation fluctuations like trading stocks (which would be “mark-to-market accounting”).

Therefore, even if OpenAI’s post-IPO valuation hits $1 trillion, Microsoft cannot add hundreds of billions to its balance sheet overnight.

Conversely, under the equity method, Microsoft’s financial reports are directly tied to OpenAI’s actual operational performance.

Specifically, at each quarterly settlement, Microsoft first looks at how much money OpenAI earned or lost that quarter;

Then, based on its shareholding percentage, it records that portion of profit or loss directly into its own “Other Income/Expense” line item;

In other words, OpenAI’s performance directly impacts Microsoft’s net profit.

The formula might be more intuitive:

This accounting treatment is actually quite common, typically used for investments where the stakeholder holds a significant share but lacks controlling interest.

Once you understand this logic, things get interesting.

Sharp-eyed netizens realized that using Microsoft’s “equity method” calculation, one can reverse-engineer OpenAI’s true financial status from last quarter.

Known: Microsoft reported a $3.1 billion reduction in its financials due to losses from its OpenAI investment;

Also Known: According to disclosures on OpenAI’s organizational restructuring this week, Microsoft currently holds a 27% stake.

A simple arithmetic problem reveals a shocking secret:

OpenAI’s net loss last quarter was $11.5 billion!

I think the $11.5B figure relies entirely on the accuracy of the 27% ownership disclosure and assumes no other complex equity adjustments. From the paper, equity method accounting reflects operational losses, not market sentiment, so a high valuation does not offset this burn rate on the balance sheet.

The $11.5 Billion Question: Why OpenAI’s Losses Are a Feature, Not a Bug

The core technical claim here is that OpenAI’s reported $11.5 billion net loss is primarily driven by capital-intensive R&D and compute expenditures necessary to maintain State-of-the-Art (SOTA) status, rather than operational inefficiency. This would be falsified if the company’s Annualized Run Rate (ARR) of $12 billion failed to cover its variable costs for model serving, rendering the current “Prisoner’s Dilemma” strategy economically unsustainable in the short term.

The IPO Valuation Paradox

Upon reading this report, I followed the public reaction closely. Many observers awaiting OpenAI’s IPO expressed skepticism regarding the valuation:

They lost $110 billion, yet they want to tell us at the IPO that the company is worth over $1 trillion. Haha…

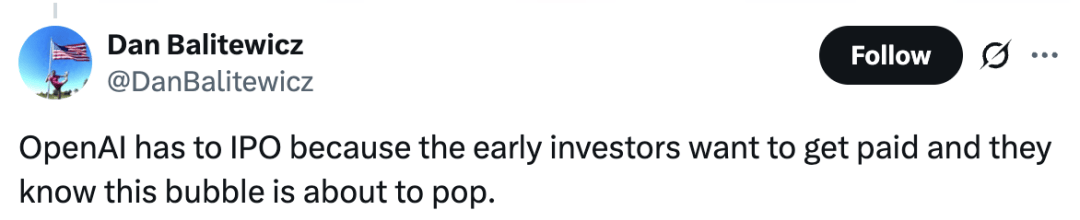

Some commentators suspect the timing is designed for early investors to exit before a potential market correction:

OpenAI must go public as soon as possible because early investors want to cash out and exit. They know this bubble is about to burst.

One caveat: the assumption that a $1 trillion valuation is detached from fundamentals ignores the strategic value of proprietary model access to Microsoft’s ecosystem. I think labeling this a “bubble” assumes open-source alternatives will immediately erode OpenAI’s pricing power, which current data does not support.

Revenue vs. R&D: The Real Picture

Contrary to the headline narrative, OpenAI is not “losing” money in a traditional operational sense. While the books show a shortfall exceeding $10 billion, this reflects the industry-wide “Prisoner’s Dilemma” rather than business failure. According to Information, OpenAI’s revenue approximately doubled in the first seven months of this year, reaching an Annualized Run Rate (ARR) of $12 billion.

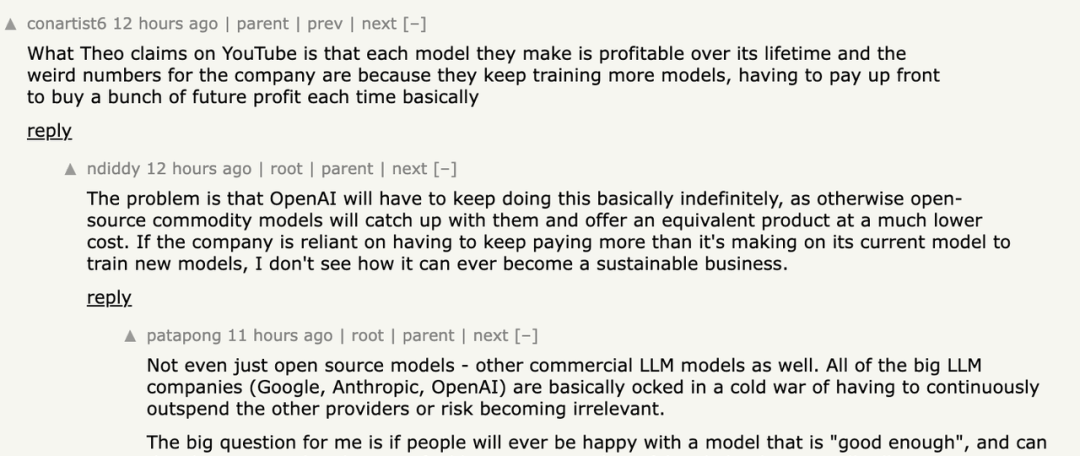

This implies earnings of roughly $1 billion per month from subscriptions and API usage alone. Even accounting for exorbitant training costs, these figures suggest a viable underlying business model. Netizens correctly identified that the financial anomaly stems from continuous model training:

The reason for OpenAI’s financial anomaly lies in their continuous training of more models.

From the paper, the analysis relies on ARR as a proxy for stability, which may overstate sustainability if churn rates increase during economic downturns. One caveat: assuming all released models are profitable throughout their lifecycle ignores the high marginal cost of maintaining legacy model infrastructure.

The SOTA Arms Race

The driver behind these expenditures is clear: OpenAI must maintain its SOTA position to prevent open-source models from overwhelming its commercial brand. In the foundational model segment, user stickiness is low; substitutes appear instantly. This has created a “Cold War” among major players like Google, Anthropic, and xAI, where companies burn capital on compute and time just to stay ahead.

Open-source models may not have visibly taken market share yet, but they exert immense pressure on cost structures through externalities. However, rigorously speaking, this book loss does not equate to operational insolvency. From an economic perspective, if revenue covers “amortized R&D expenses of models under development + daily operational costs,” the company remains viable. The capital is already spent; as long as variable costs are covered via APIs and subscriptions, there is reason to continue.

The Microsoft Strategic Imperative

The situation resembles a shipping company borrowing for vessels: as long as freight covers crew wages and fuel, the business continues even if loan principal isn’t repaid yet. Similarly, Microsoft’s concern with OpenAI’s profitability is secondary to its strategic need for access to the industry’s strongest models. To keep this advantage, Microsoft must continue funding OpenAI’s R&D and compute needs.

Simply put, the relationship is defined by Microsoft paying for infrastructure while OpenAI focuses on:

The Economics of Burning Cash

I read the latest financial disclosures, and the headline number is stark: OpenAI reported an $11.5 billion net loss in its most recent quarter. What stands out isn’t just the magnitude of that deficit, but how Microsoft frames it not as a failure of investment, but as a necessary infrastructure subsidy. The core technical claim here is that massive compute expenses are being absorbed by Azure to secure long-term enterprise dominance. This would be falsified if OpenAI’s model performance did not justify the staggering capital expenditure required to keep them in the game.

So, although the “little brother” caused the big brother’s book value to drop by $3.1 billion last quarter, this is less a bad debt and more of a strategic subsidy initiated by Microsoft. Even if it were truly a “mess,” considering Microsoft earned a net profit of $27.7 billion last quarter, losing a mere 3.1 billion is just a drop in the bucket.

I think the assumption that Azure will capture all future compute spend ignores potential multi-cloud strategies OpenAI might adopt to reduce vendor lock-in risks.

Furthermore, the massive compute expenses OpenAI incurs will ultimately flow back into Microsoft’s Azure cloud. According to the latest cooperation agreement, OpenAI has committed to purchasing an additional $250 billion worth of Azure cloud services in the future.

From the paper, a $250 billion commitment is a staggering figure that assumes linear scaling of compute demand, which may not hold if model efficiency improves drastically.

In summary, Microsoft’s “loss” does not indicate that there is a problem with OpenAI; rather, it demonstrates that—within AI R&D of this scale—subsidies at the infrastructure level have become necessary. As one netizen put it, the rules of the AI game have long changed: from “who can build the best model” to “who can survive longer while burning cash.”

One caveat: this narrative obscures the lack of clear revenue pathways for OpenAI itself, shifting focus entirely to Microsoft’s balance sheet resilience.

While Snipe and Clam Struggle, Old Huang Profits

The core technical reality here is the divergence of capital efficiency: OpenAI’s burn rate has decoupled from its revenue generation, while Nvidia’s hardware monopoly ensures positive cash flow regardless of software adoption curves. This dynamic would be falsified if OpenAI demonstrated a clear path to profitability that didn’t rely on infinite scaling of inference costs or if Nvidia’s market cap corrected due to supply chain constraints rather than demand speculation.

Investors remain polarized on whether the current AI infrastructure spend constitutes a speculative bubble, yet Nvidia’s market capitalization has cleanly surpassed five trillion dollars. The data suggests an inverse correlation in this specific quarter: the harder OpenAI loses money, the more “Old Huang” (Jensen Huang) profits.

I read the financial filings and followed the market reaction; what stood out to me is the structural safety Nvidia holds. Even if OpenAI’s $11.5 billion net loss validates the “bubble” thesis, Jensen Huang’s position remains insulated because he sells the shovels during the gold rush, regardless of whether anyone finds gold.

I think the assumption that inference costs will scale linearly with model size ignores potential algorithmic breakthroughs in efficiency. From the paper, nvidia’s dominance relies on CUDA lock-in, which may not hold if open-source alternatives gain sufficient enterprise traction.

Comments

Sign in to join the discussion and leave a comment.

Sign in with Google