The core technical claim here is a commercial scaling law: compute and revenue are moving in lockstep, suggesting that throwing more capital at infrastructure yields proportional financial returns. This would be falsified if we saw diminishing marginal returns on compute spend—where revenue growth stalls despite exponential increases in GPU capacity—or if the reported ARR figures prove to be non-recurring or accounting-heavy rather than sustainable subscription income.

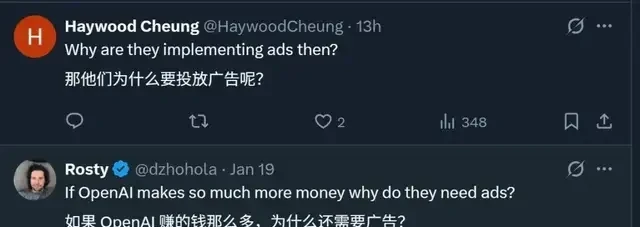

OpenAI has released data that initially seems to contradict its recent pivot toward advertising, a move driven by public criticism of its financial constraints. The numbers are undeniably large: Annual Recurring Revenue (ARR) has surged from $2 billion two years ago to $20 billion.

Furthermore, the company highlights a direct correlation between resource expenditure and income growth. Between 2023 and 2025, computing capacity increased by a factor of 9.5, while revenue grew tenfold. This suggests that in the current AI market, scale is not just an engineering challenge but a primary driver of monetization efficiency.

These figures originate from an announcement by OpenAI’s Chief Financial Officer, rather than an independent audit. The precision of these projections implies a level of certainty in long-term enterprise contracts that is rare for hardware-intensive startups.

I think tenfold revenue growth on 9.5x compute suggests high-margin software layers are absorbing the infrastructure costs effectively. I remain skeptical of ARR figures that exclude churned users or heavily discounted enterprise pilot programs.

This financial transparency has sparked confusion among observers: if earnings are this substantial, why is OpenAI pursuing the widely criticized strategy of displaying ads? The public discourse assumes that high revenue should eliminate the need for ad-supported tiers, ignoring the complexity of capital allocation in deep tech.

The answer provided is straightforward but stark: although earnings are high, expenditures are equally massive. The cost of maintaining and expanding this compute cluster likely dwarfs the net profit, explaining the need for diverse revenue streams including advertising to sustain operations.

From the paper, without a breakdown of OpEx versus CapEx, “massive expenditures” remains an unverified assumption. One caveat: ad revenue is likely negligible compared to enterprise contracts; its inclusion here may be for user acquisition rather than profit.

As public discussion intensifies regarding OpenAI’s revenue model, new details have also surfaced about the company’s first hardware product. An OpenAI executive stated that its inaugural device is likely to launch in the second half of 2026. This timeline suggests a deliberate separation between their software scaling and physical product rollout, prioritizing cloud infrastructure dominance before entering the consumer hardware market.

More Compute, More Revenue: OpenAI Validates AI Commercial Scaling Law

The Flywheel Logic and the Burn Rate Reality

The core technical claim here is that OpenAI has empirically validated a commercial scaling law: compute investment drives model capability, which drives revenue, which funds further compute. If this loop were to break—meaning revenue growth decouples from compute expansion despite continued spending—the premise of their current capital strategy would be falsified.

OpenAI explicitly frames this as a self-reinforcing cycle:

Investments in computing power drive leaps in research and model capabilities. Powerful models lead to better products and broader adoption, which in turn drives revenue growth. This revenue then supports the next round of computing investments and innovation. This cycle continues to strengthen.

I read through their recent statements regarding the controversial introduction of ads into ChatGPT. While I won’t rehash the public outcry, the underlying financial logic remains stark: the more computing power OpenAI has, the higher its total revenue, creating a continuous drive for technological innovation.

I think the assumption that model capability linearly translates to user adoption ignores the saturation of current consumer use cases. From the paper, this scaling law assumes no regulatory or infrastructure bottlenecks will interrupt the compute supply chain.

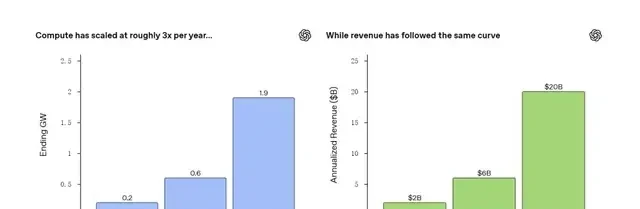

The data supports this trajectory, albeit with aggressive growth metrics:

- 2023: Computing power 0.2 GW; ARR (Annual Recurring Revenue) $2 billion

- 2024: Computing power 0.6 GW; ARR $6 billion

- 2025: Computing power 1.9 GW; ARR exceeding $20 billion

Between 2023 and 2025, OpenAI’s computing capacity grew by a factor of 9.5, and revenue followed a similar growth curve, increasing threefold year-over-year and tenfold over the three-year period.

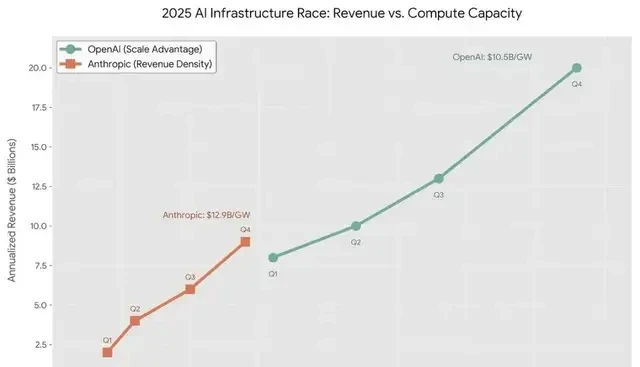

To contextualize this scale, I compared OpenAI with its primary competitor, Anthropic (parent company of Claude):

It is evident that OpenAI’s overall scale is significantly larger than that of its competitor. However, under this flywheel effect, while OpenAI earns more, it also burns through cash even faster…

One caveat: comparing ARR directly without accounting for differing cost structures between API-heavy and consumer-heavy models is misleading. I think the “flywheel” assumes compute costs remain stable relative to revenue, which historical hardware trends suggest is unlikely.

To date, although OpenAI has established cloud service partnerships with Microsoft and Oracle, considering long-term future needs, it has begun investing heavily in building its own AI data centers. Starting from late last year, the company has collaborated with manufacturers such as NVIDIA, Oracle, and SoftBank to advance GW-scale data center projects across multiple fronts.

Regardless of how costly self-building is, just looking at previously disclosed bills for renting cloud computing power reveals how quickly money can be spent. In October 2025, statistics provided by Epoch AI showed that—OpenAI spent a total of $7 billion on computing resources in 2024, with this astronomical bill paid almost entirely through renting cloud computing power from Microsoft. Note: This figure does not include upfront investments in data centers.

Therefore, to maintain the flywheel OpenAI envisions, whether $20 billion in ARR is sufficient remains uncertain. Given the increasingly critical role of computing power, revenue may ultimately be, as netizens suggest:

Merely a natural result of expanded computing capacity.

Monetization Strategies Beyond the API

According to OpenAI’s logic, there is another crucial link between computing power and revenue: powerful models and products. After all, more applications lead to higher revenues…

Explaining why the company rolled out ads across its platform, OpenAI’s CFO stated:

Business models should expand in tandem with the value created by intelligence.

Initially, ChatGPT was free. However, as users demanded greater capabilities and reliability, subscription services were introduced accordingly. Simultaneously, to enable developers and enterprises to embed intelligence into their systems via APIs, OpenAI built a platform-based business model. The introduction of ads aims further to help users with decision support in commercial and transactional scenarios.

In the future, beyond ad revenue, the company will continue to drive growth through tiered subscriptions and usage-based API pricing (tied to production workloads). Furthermore, as agents penetrate fields such as scientific research, drug discovery, energy systems, and financial modeling, new business models will emerge.

First Hardware Product Expected to Launch This Year

The core technical claim here is that OpenAI’s commercial scaling law—more compute driving more revenue—is directly accelerating their physical product roadmap. If the second-half 2026 launch date slips significantly, it would suggest that hardware integration remains a bottleneck unrelated to pure computational throughput.

Chris Lehane, Chief Global Affairs Officer, recently stated that the company is “on track” to launch its inaugural device in the second half of 2026. He also teased that more details would be shared later this year.

Multiple leaks suggest that this hardware is likely a screenless AI smart pen, described in form factor as being comparable in size to an iPod Shuffle.

Earlier, OpenAI CEO Sam Altman made a peculiar comment:

When the design is “right,” users will want to bite it.

Hmm… based on the description, it does seem, perhaps, possibly like a pen?

One caveat: screenless devices often fail to capture user attention because they lack immediate visual feedback loops. I think the iPod Shuffle comparison suggests a focus on portability over functional complexity. From the paper, relying on leaked form factors introduces significant uncertainty into any launch timeline analysis.

Regardless, with the latest information released, we now know that this hardware’s debut is drawing closer. After all, the commitment previously given by Altman and Jony Ive was: complete the launch within two years. When they mentioned the two-year timeline before, outsiders speculated that their hardware development was facing difficulties due to a lack of computing resources. Now, with the timeline (at least in perception) shortening, it is reasonable to infer that this is also related to computing power. Indeed, increased revenue → expanded computing power → faster hardware rollout fits perfectly into the cycle.

Comments

Sign in to join the discussion and leave a comment.

Sign in with Google