The burden of proof has shifted from speculative promise to concrete capital allocation. With OpenAI securing $110 billion, the accountability for governance now rests with the consortium of tech giants backing this valuation. I read the filing details closely: SoftBank, Nvidia, and Amazon are not just investors; they are infrastructure partners defining the operational limits of this new entity.

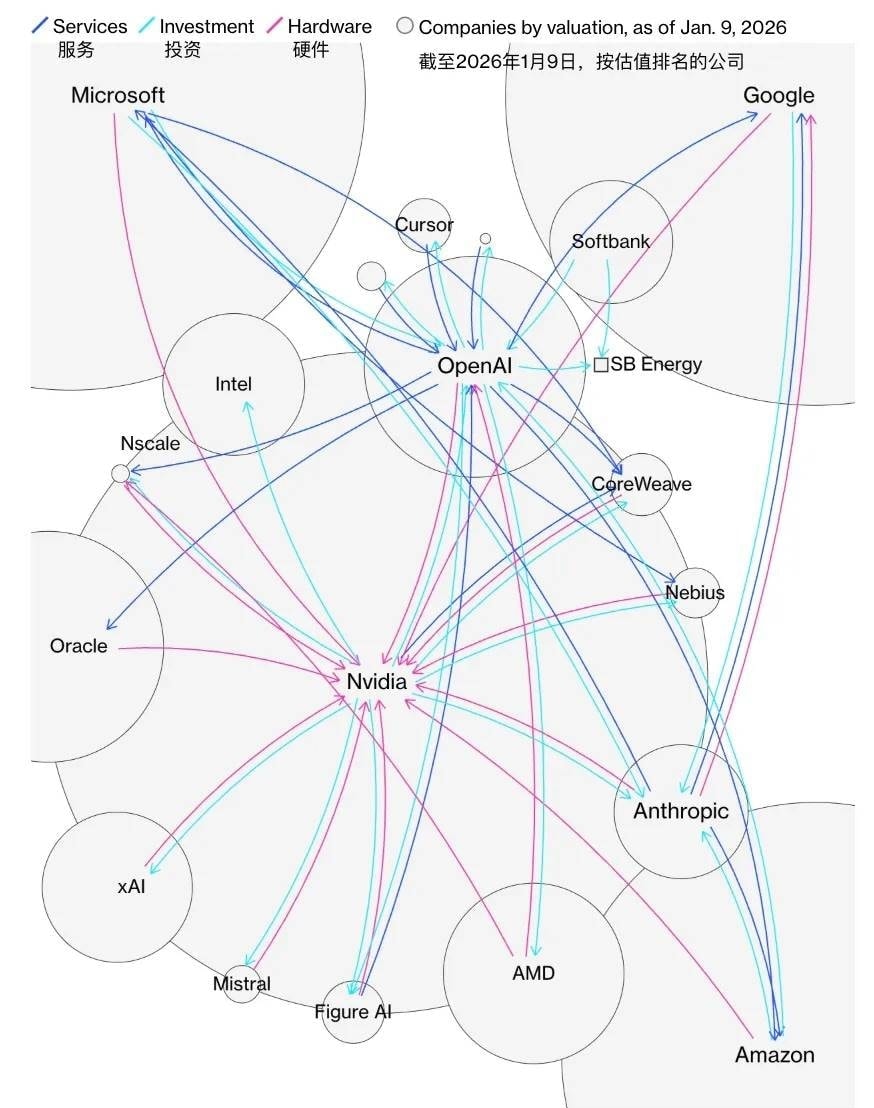

On February 27, OpenAI announced it had raised $110 billion in new funding. The round includes $30 billion from SoftBank, $30 billion from Nvidia, and $50 billion from Amazon, valuing the company at $730 billion pre-money. This marks the largest single financing deal to date in the AI sector.

Officially, the funds will be used to expand artificial intelligence infrastructure construction, accelerating the democratization of AI. Sam Altman outlined the specific areas of cooperation with the three partners on X:

- Nvidia: Responsible for providing underlying computing power, offering continuous and scalable training and inference capabilities for OpenAI centered around GPUs and next-generation accelerators;

- Amazon: Providing cloud infrastructure and global deployment capabilities to support model delivery and commercialization across multiple regions and industry scenarios for OpenAI;

- SoftBank: Assuming a greater role in capital and ecosystem integration, driving OpenAI’s expansion into broader industrial systems through long-term financial support and resource consolidation.

I think the tripartite structure creates a closed loop of compute, cloud, and capital that is difficult to regulate externally. Enterprises must verify which compliance standards apply when infrastructure providers also hold equity in the model developer. We should watch for antitrust scrutiny regarding this vertical integration.

Additionally, as an existing shareholder of OpenAI, Microsoft did not miss out. The two parties released a joint statement confirming that their previous cooperative relationship remains unaffected. Microsoft Azure continues to serve as the exclusive cloud service provider for OpenAI’s API, and Microsoft retains exclusive licensing and access rights to the intellectual property within OpenAI’s models and products.

At this moment, three of the most critical AI resource lines—upstream computing power, cloud infrastructure, and long-term capital—have been tied together in a single move.

OpenAI’s $110B Round Stokes IPO Talk as Private Valuation Nears $800 Billion

One Financing Round to Bind Three Giants

The burden of proof now shifts to the board and its major backers: can OpenAI justify an $800 billion valuation while tying its future to specific technical milestones? I read the terms closely, and the structure reveals a high-stakes dependency on both AGI achievement and market liquidity.

In this latest financing round, Amazon emerged as the most significant investor, committing $50 billion. The capital injection is structured in phases: an initial $15 billion deployment, followed by an additional $35 billion contingent upon specific conditions within the next few months. While the filing does not explicitly define these triggers, insiders indicate they likely involve OpenAI “achieving AGI” or a successful IPO.

This creates a precarious governance dynamic. Furthermore, a special clause in the existing cooperation agreement between OpenAI and Microsoft stipulates that once AGI is achieved, Microsoft will lose access to its technology. This effectively severs a critical strategic partnership at the very moment of technological maturity.

Under the new agreement with Amazon, OpenAI plans to develop a “stateful runtime environment,” hosting its models on Amazon’s Bedrock platform. The company has committed to consuming large-scale cloud computing resources on AWS, including approximately 2 gigawatts of Trainium chip compute power, to support Frontier, stateful environments, and other advanced workloads.

Additionally, both parties will expand upon the $38 billion agreement signed last November. Over the next eight years, OpenAI plans to consume a cumulative total of approximately $100 billion in cloud computing resources on AWS. Amazon CEO Andy Jassy stated, “Today, the world’s two largest AI labs are heavily utilizing Trainium.” Besides OpenAI, the other is Anthropic.

Previously, Amazon had invested billions into Anthropic and built an $11 billion data center campus in Indiana, known as the “Project Rainier,” specifically for training and running Anthropic’s models. However, Amazon also clarified that its partnership with OpenAI will not alter its relationship with Anthropic.

The second investor is Nvidia. In September last year, rumors circulated that Nvidia would invest $100 billion in OpenAI. However, subsequent reports suggested the investment amount might be smaller. At the time, Jensen Huang (Jensen “Old Huang”) specifically stepped out to debunk claims that “Nvidia was abandoning OpenAI”:

We are putting significant capital behind them; I believe in OpenAI. The work they are doing is incredible.

And now, just like that, $30 billion has arrived. Under this agreement, OpenAI commits to using 2 gigawatts of training capacity on Nvidia’s Vera Rubin system, with an additional 3 gigawatts of computing resources (likely in the form of GPUs) dedicated to running specific AI inference tasks.

In other words, Nvidia serves as both a strategic investor and its chip supplier for OpenAI—effectively funding OpenAI to buy its own chips. This represents another logic of “circular investment.”

The third investor is SoftBank, contributing $30 billion. Official announcements indicate that SoftBank’s investment will be disbursed in three installments in April, July, and October 2026.

SoftBank Group Chairman and CEO Masayoshi Son expressed confidence in OpenAI’s continued growth:

Through this additional investment, we will accelerate OpenAI’s research and ecosystem expansion while advancing our own AI strategy.

Notably, some media outlets suggest SoftBank plays not only the role of an investor but also a “matchmaker.” Insiders indicate that OpenAI is expected to secure approximately $10 billion in further primary equity financing, with related commitments to be finalized within the next month. Investors include sovereign wealth funds and investment firms. It is speculated that these investors may connect through SoftBank.

My read: The AGI condition for Amazon’s tranche creates a binary risk event for shareholders. My read: Microsoft losing access post-AGI undermines their long-term strategic alignment. My read: Nvidia’s circular funding model ties OpenAI’s hardware costs to its equity value.

OpenAI’s $110B Round Stokes IPO Talk as Private Valuation Nears $800 Billion

Microsoft Relationship Remains Intact, but Diversification Sought

I followed the release closely, and while the headline is the valuation, the governance reality is the shifting dependency matrix. The burden of proof now lies with OpenAI to demonstrate that this “diversification” isn’t just a hedge against Azure’s pricing power, but a genuine architectural shift.

Microsoft remains OpenAI’s largest shareholder and exclusive infrastructure partner for stateless APIs. Despite market speculation following the new financing round, both entities reaffirmed their partnership’s “core status”:

- Exclusive Status of Azure: Microsoft Azure continues as the sole cloud provider for OpenAI’s stateless API. First-party products, including Frontier models, remain hosted on Azure.

- Unchanged Commercial Logic and Revenue Sharing: The existing revenue-sharing agreement holds firm. Even if OpenAI generates revenue via Amazon or Oracle clouds, Microsoft retains its “cut.”

- Intellectual Property Exclusivity: Microsoft maintains exclusive licensing rights to the IP of OpenAI’s current models and future products.

However, this financing round signals a strategic pivot toward business diversification beyond its long-standing reliance on Microsoft.

Amazon’s entry is the clearest indicator. As a direct competitor to Microsoft in cloud computing, Amazon’s inclusion—coupled with OpenAI’s commitment to an additional $100 billion in AWS consumption over eight years and large-scale adoption of Amazon’s self-developed Trainium 3/4 chips—shows OpenAI is unwilling to concentrate all its compute risk on Azure.

My sense is enterprises must verify if Microsoft’s IP exclusivity clauses restrict their ability to deploy these models on alternative clouds for compliance reasons. What concerns me is that the revenue-sharing model suggests Microsoft benefits regardless of where inference happens, reducing the incentive for true infrastructure independence.

One More Thing

At this point, it is difficult to ignore what appears to be a “circular financing” structure.

Nvidia acts as both shareholder and sole supplier of underlying computing power (“the arms dealer”); Amazon serves as both new investor and future cloud provider.

Simply put, suppliers (Nvidia/Amazon) invest capital into their customer (OpenAI), who then uses that capital to purchase chips or cloud services from those same suppliers. For the suppliers, this capital shifts on their balance sheets from “investment expenditure” to “operating revenue,” boosting stock prices while locking in future market share.

It is a win-win situation for the investors and OpenAI, but it raises questions about financial transparency and dependency.

Although outside observers have raised concerns about this “circular financing” narrative, Sam Altman addressed it directly:

I understand everyone’s concerns; this only makes sense when new revenue flows into the entire AI ecosystem.

OpenAI’s previous funding round closed in March 2025, raising $40 billion and valuing the company at $300 billion—the largest private equity financing deal in history at that time.

With this new round added to existing cash reserves of approximately $40 billion, OpenAI’s available funds will increase to approximately $150 billion. The company expects to achieve positive free cash flow for the first time only by 2030.

OpenAI clearly needs these funds and computing resources. Data from February shows that ChatGPT’s weekly active users have surpassed 900 million, with monthly visits reaching approximately 57.2 billion. There are over 50 million individual subscribers and more than 15,000 active enterprise customers.

Altman also noted he is dedicating significant effort to securing additional computing capacity to meet the demand for ChatGPT and other OpenAI products.

Competition among top AI laboratories remains fierce. Recently, rival Anthropic secured $30 billion in funding from investors including Microsoft and Nvidia, pushing its post-money valuation toward $380 billion and enhancing its ability to compete with OpenAI.

Now that the ammunition is loaded, we will see what surprising new models OpenAI brings to the table with this massive influx of capital.

I think the 2030 cash flow target suggests enterprises should not assume near-term profitability or price stability for these services. My sense is governance teams must scrutinize whether circular investments create hidden conflicts of interest in procurement decisions.

Comments

Sign in to join the discussion and leave a comment.

Sign in with Google